When the United States moves toward direct confrontation with Iran, the easy story is to treat the crisis as a test of military resolve — who has the carrier groups, who has the missiles, who is willing to strike first, harder, and longer. That story is incomplete.

Real geopolitics is never just about firepower. It is not just about global finance either. It is not just about one political leader, one ideology, or one economic interest. It is a smorgasbord of competing pressures, overlapping institutions, old alliances, domestic fears, commercial exposure, and strategic calculation.

Britain's response to the Iran crisis made that clear. Prime Minister Keir Starmer said the United Kingdom was not involved in the strikes on Iran, even while Britain supported limited defensive actions in the region. Close to the United States, but not fully inside America's war footing. That hesitation was not random. It reflected Britain balancing alliance politics, regional security, domestic inflation, energy vulnerability, and the role of London as a global center of marine insurance and financial risk pricing. That is what makes this story worth examining — not one hidden lever, but many levers being pulled at once.

Britain's Position Was Neither Neutral nor Fully Committed

Britain did not stand aside entirely, but it also did not fully jump aboard America's offensive posture. Starmer publicly said the UK was not involved in the strikes on Iran, while the government separately described British participation in terms of specific and limited defensive action tied to Iranian regional attacks. That difference matters.

Britain wanted to preserve the alliance with Washington without immediately owning the full political, military, and economic cost of escalation. That is how states behave when they are allied to a stronger power but exposed to different risks. The UK economy is more vulnerable to oil shocks, inflation, and borrowing pressure than American political rhetoric sometimes acknowledges. But Britain's caution went deeper than inflation headlines alone.

- Treaty alliance obligations and NATO solidarity

- Shared intelligence and security interests in the region

- Long-term relationship with Washington as strategic anchor

- Deterrence credibility requires visible allied commitment

- Greater exposure to oil shocks and energy price inflation

- UK borrowing costs rising as inflation fears mounted

- London marine insurance market directly in the firing line

- Domestic political blowback from higher fuel and living costs

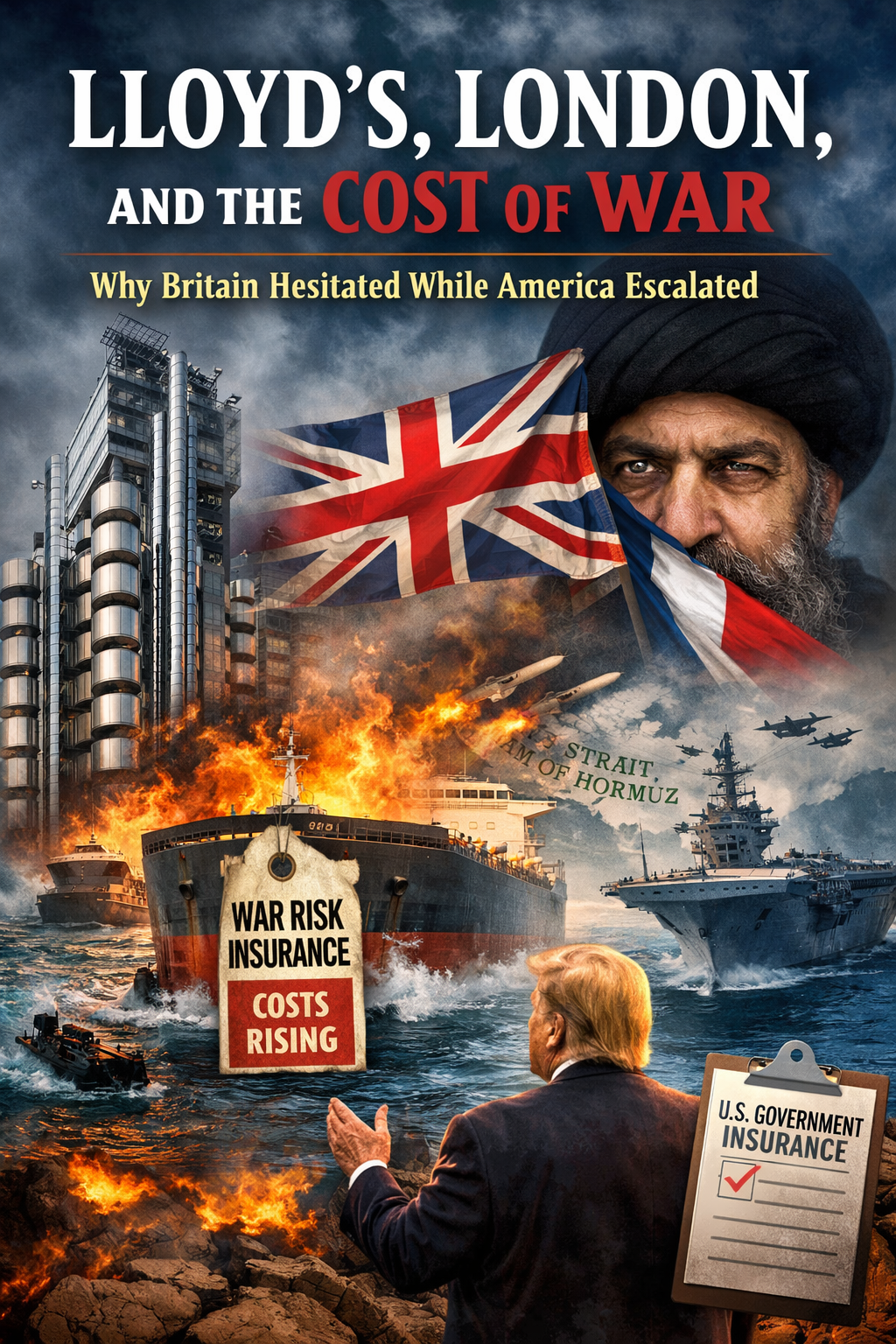

Lloyd's of London Sits at One of the Pressure Points of War

When people think about war, they think about armies, airstrikes, and headlines. What they often miss is how quickly conflict becomes a question of shipping, insurance, and exposure. That is where Lloyd's of London enters the picture.

Lloyd's and the wider London marine insurance market help determine what it costs to move ships through dangerous waters. When conflict intensifies in the Gulf, underwriters widen high-risk zones, reprice exposure, and adjust war-risk coverage. London's marine insurance market widened the high-risk area in the Gulf as the conflict escalated.

A war in the Gulf is not just a military contest. It is a freight contest. An energy contest. An inflation contest. A contest over who absorbs risk and who pays to keep commerce moving. The moment Lloyd's reprices danger, the crisis changes form — missiles are still flying, but now insurers, charterers, traders, and governments are all reacting to the same danger in different ways. That is what makes geopolitics so messy. No single interest gets to dictate the whole picture.

Washington Was Not Just Thinking Militarily

The American side of this equation was not limited to bombs and threats. Lloyd's was engaging with the U.S. International Development Finance Corporation over a plan to provide political-risk insurance and guarantees for maritime trade in the Gulf. Washington was not merely trying to defeat Iran militarily — it was also exploring how to stop commercial fear from choking off shipping and magnifying the economic damage of the conflict.

Firepower may win battles, but insurance, oil flows, and commercial confidence shape how costly a conflict becomes — and how long the political system can sustain it.

London's insurance market was translating danger into price. Washington was looking for ways to keep price from becoming strategy's veto. That is not a side issue. That is part of the war.

Britain's Hesitation Was the Product of Competing Interests

Britain's position only looks confused if one assumes geopolitics is supposed to be simple. It is not. Britain had reasons to support the United States. It also had reasons to fear the economic consequences of a wider conflict — to reassure allies in the region while limiting domestic blowback from higher energy costs, higher inflation, and tighter financial conditions. Britain wanted major economies to consider releasing emergency oil reserves to blunt the shock from the crisis, while London markets reflected renewed inflation fears as oil prices surged.

That is what states do. They balance. They hedge. They posture. They adapt. They try to preserve room to maneuver while protecting the interests that matter most at home. The old temptation is to explain this kind of behavior through a single master theory.

Finance runs everything. Or military power runs everything. Or ideology runs everything. Or one leader's will runs everything. Pick your preferred villain and build the story around it.

Alliance commitments, economic vulnerability, insurance markets, domestic politics, and strategic calculation all collided in the same moment — each pushing Britain in a slightly different direction.

Britain's response made sense precisely because it was shaped by many pressures at once.

The Union Jack and the Mullah's Beard

There is an old saying that if you look under the beard of a mullah, you will find a Union Jack. Taken literally, it is too cartoonish to carry much weight. But it survives because it hints at something historically familiar: Britain has long tried to influence the Middle East not only through open power, but through commercial leverage, selective alignment, intermediaries, and distance.

That instinct did not disappear when empire faded. It changed form. Modern Britain does not command the region. But London still matters in quieter ways — through diplomacy, alliance management, finance, and the pricing of risk. Britain still occupies important chokepoints in the system through which events are interpreted, managed, and financed. That is a more serious point — and a more believable one — than any story about secret control.

Geopolitics Is a Smorgasbord

The deeper lesson here is bigger than Britain, Iran, or Lloyd's. Geopolitics is not just about which country has more weapons, who dominates global finance, whether one leader is bold or weak, or which ideology is winning. It is all of those things at once, colliding with one another.

Want freedom of action — the ability to strike, threaten, and maneuver without commercial or political constraint.

Want risk priced properly — premiums that reflect the actual danger of transiting a war zone, regardless of political convenience.

Want inflation contained, allies reassured, and domestic political blowback minimized — often in direct tension with military objectives.

Want predictability — stable oil flows, manageable risk, and a clear sense of where the crisis ends.

Wants the region to feel too dangerous and too expensive to navigate — using market fear as a strategic weapon.

Want victory without domestic backlash — which means managing the story as much as managing the conflict itself.

No single actor owns the whole board. Britain hesitated because it was sitting at that table with its own set of interests. America pushed ahead because it was sitting at the same table with a different set. Lloyd's mattered because it sits near one of the places where military danger becomes financial consequence.

My Bottom Line

The Iran crisis showed that power does not move in a straight line. Britain's hesitation was not simply cowardice. It was not simply disloyalty. It was not simply the work of finance, or the product of one politician's caution. It was what happens when alliance commitments, economic vulnerability, insurance markets, domestic politics, and strategic calculation all collide in the same moment.

That is the real shape of geopolitics. It is not one force. It is many. And that is why the most honest way to understand Britain's response is not through a single explanation, but through the recognition that global affairs are a smorgasbord of competing interests — each powerful enough to matter, none powerful enough to explain everything by itself.

Wars are fought not only through missiles and speeches, but through shipping lanes, premiums, inflation, diplomacy, domestic politics, and alliance management. The world is rarely run by one thing. It is usually pushed and pulled by many things at once.

References

- PM statement on Iran: 1 March 2026. GOV.UK.

- Summary of the UK Government legal position: The legality of defensive action in respect of Iranian regional attacks. GOV.UK.

- UK seeks to limit economic hit from Iran as borrowing costs jump. Reuters, March 9, 2026.

- London marine insurers widen high-risk zone in Mideast Gulf as conflict escalates. Reuters, March 3, 2026.

- Maritime insurance premiums surge as Iran conflict widens. Reuters, March 6, 2026.

- Lloyd's market engaging with U.S. government over Gulf maritime plan, officials say. Reuters, March 5, 2026.

- London's FTSE indexes fall as oil prices soar, inflation concerns mount. Reuters, March 9, 2026.

- Middle East crisis likely to push UK inflation up, Rachel Reeves tells MPs. Financial Times, March 10, 2026.

- UK inflation likely to rise because of Middle East war, says Rachel Reeves. The Guardian, March 9, 2026.

Disclaimer: The views expressed in this post are the personal opinions of the author and are offered for educational, commentary and public discourse purposes only. They do not represent the positions of any institution, employer, organization or affiliated entity. Nothing in this post constitutes legal, financial, medical or professional advice of any kind. References to public figures, institutions, historical events and current affairs are based on publicly available sources and are intended to support analysis and argument, not to state facts about any individual's character, intent or conduct beyond what the cited sources support. Commentary on religious, political and cultural subjects reflects the author's independent analysis and is protected expression of opinion. Readers are encouraged to consult primary sources and form their own conclusions. Any resemblance to specific individuals or situations beyond those explicitly referenced is coincidental.